Planning for IAS Coaching? Know about Education Loan

Quality education is essential for a successful and complete life. For most people, it is almost like graduating from a recognized institution. It is well known that the education cost is expensive and increasing rapidly. Moreover, the cost of learning at top universities and colleges is also quite expensive in recent years.

Parents, ensure to keep this in mind and offer your child the best education by investing your money in fixed deposits, mutual funds, unit-linked insurance plans, etc. for the long term. For instance, if you have a dream of seeing your child as an IAS officer, it is essential for you to give quality foundation education, higher education, and also IAS coaching from top IAS Coaching Centres in Chennai. It is not an easy thing to provide education for all these by just depending on your earnings. It is best to invest in various forms like fixed deposits, mutual funds, or other associated investment plans.

However, some people will experience a fund shortage in spite of investing in all this. In such a scenario, it is recommended to take an education loan. It helps to bridge the space between the required amount and the shortfall. To know more, click here.

As per studies, the education cost is increasing by about 15% per year on an average basis. The cost of MBA studies has been increased from INR 2.5 lakhs to INR 20 lakhs in two decades. If a couple is investing INR 2,000 per month for 15 years, they can save approximately INR 9.5 lakhs on an average basis.

What are the coverage and benefits of educational loan?

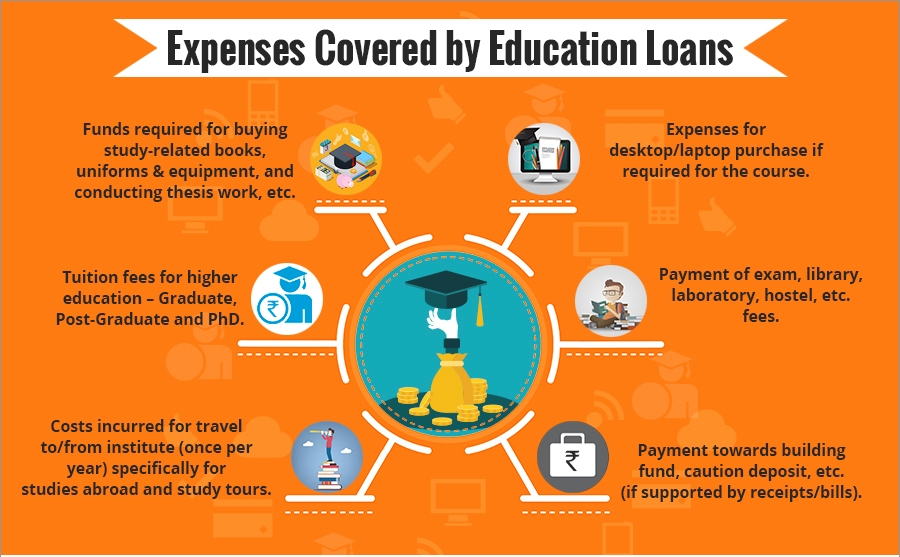

The education loan helps cover the basic course charge and other associated expenses like an exam, accommodation, and additional necessary charges.

Who is eligible to apply for an educational loan?

The main borrower for an educational loan is the student. A sibling, spouse, or parent can remain as co-applicant.

To whom the educational loan is provided?

It is provided to students who are interested in studying higher education in overseas or India. The maximum provided as loan to students who study in India or other foreign countries differs. It depends upon the bank that is offering the loan. It is recommended to check with the bank regarding loan amount and interest rates.

What are the kinds of courses enclosed under the educational loan?

It is possible to take educational loan for a vocational course, part-time course or full-time course and post graduation or graduation in the area of management, engineering, hotel management, medical, architecture, etc.

Documents necessary and eligibility criteria

To apply for an educational loan, the student should be an Indian citizen. He/she should have obtained admission into a university or college that is recognized by a leading authority in abroad or India. The student should have accomplished higher secondary schooling.

Some banks provide finance even before the student has got admission in the university. According to the RBI or Reserve Bank of India guidelines, there are no strict restrictions for upper age limit, however certain banks have a maximum age limit for an educational loan. The bank request for certain vital documents like institution admission letter, Class XII, Class X, and graduation mark sheets and fees structure. It is also essential to submit income documents like ITR (income tax returns) or salary slips of the co-applicant.

Bank of India guidelines, there are no strict restrictions for upper age limit, however certain banks have a maximum age limit for an educational loan. The bank request for certain vital documents like institution admission letter, Class XII, Class X, and graduation mark sheets and fees structure. It is also essential to submit income documents like ITR (income tax returns) or salary slips of the co-applicant.

Collateral requirement, loan financing

Most banks will be willing to finance the entire college fees as a loan, and it mostly depends upon the amount you are applying for. At present, the majority of banks sanction the loan for up to INR 4 lakhs. There is no need to pay any margin amount. If the student is going to pursue his/her studies in India, about 5% of the loan amount should be financed. If the student is pursuing an education in foreign countries, the required margin amount is 15%.

Certain banks ask for collateral when the loan amount is more than INR 7.5 lakhs. At present, the banks do not ask for third-party guarantee or collateral for a loan within INR 4 lakhs. If the student is applying for a loan for more than INR 4 lakhs, the bank requests for third-party guarantee. The collateral is requested by banks when the loan amount is more than INR 7.5 lakhs.

After accepting the loan application, the banks will give away the amount to the university or college according to the mentioned fees structure.

Know More About : Know About Education Opportunities In Chennai